MEIEA Journal Vol 5 No 1 © 2005 Music & Entertainment Industry Educators Association All rights reserved

Papadopoulos, Theo (2005). Financial Risk and Return in the Music Recording Industry. MEIEA Journal Vol 5 No 1, 19-31.Financial Risk and Return in the Music Recording Industry

Theo Papadopoulos, Victoria University

Editor’s note: The following is presented as a reply to the preceding comment by Peter Alhadeff and Barry Sosnick (page 13).

Introduction

Alhadeff and Sosnick’s comment (hereafter, A&S) on my recent paper on the economics and equity of recoupment practices (Papadopoulos, 2004) provides an opportunity to further explore the risk and return dynamics of investment in the music recording industry. A&S make two fundamental points: the first relates to the model and the supposed omission of opportunity cost relating to the time value of money; the second relates to the equity of recoupment practices and the workability of the proposed revenue distribution model. In this reply I will refute both points and demonstrate that the model is indeed robust. Notwithstanding, A&S raise a number of important issues and highlight the need for more research into the underlying fundamentals of financial risk in the music industry. The following section details my response to the A&S critique. Thereafter, I present a discussion of further issues stimulated by the A&S comments with suggestions for future work.

Opportunity Cost and Economic Profit

The first contribution of the A&S paper is the explicit recognition of the time value of money; namely, that a recording advance has an opportunity cost measured by the foregone interest payments of an alternative investment. This is not novel and I will discuss below how this can be explicitly incorporated into the analysis. However, A&S go beyond suggesting an elaboration of the analysis to asserting that, like Papadopoulos, the existing literature proceeds as if there is no premium on the recording advance. While the general point regarding the inappropriate use of account-ing profit is valid, this criticism cannot be applied to my paper, which utilizes economic profit. The distinction between economic profit and accounting profit is that the latter includes only explicit costs while the former defines costs as incorporating both explicit and implicit costs. That is, explicit costs are actual payments made for resources (wages, rent, utilities) while implicit costs represent the opportunity cost of these same resources employed in the next best alternative use (for example, the foregone interest on the money invested by the record company and the wages foregone by the artist in pursuing a career in music). The total cost function presented in Equation 1 is indeed economic cost, as evidenced by the preceding explanation that “A construction of costs and revenues utilizing elementary microeconomic tools (emphasis added) facilitates a comparison of the firm’s breakeven sales volume to the volume of sales at which the artist is recouped” (Papadopoulos 2004, 91). Indeed, opportunity cost is explicitly discussed in the paper, for example, in the context of the relatively low success rate I state that “artists’ investment of time, money, and effort would, in economic terms, seem somewhat irrational […] The non-refundable recording advance further encourages artists since (opportunity costs aside) the financial risk is borne by the record company.” (Papadopoulos 2004, 97).

This misunderstanding arises partly from the cross-disciplinary nature of the MEIEA Journal and my own background in writing predominantly for an audience of economists. This may have been avoided with an explicit definition of economic versus accounting profit; but any student of Economics 101 should recall the distinction. Accordingly, the breakeven point as presented in my paper is accurate and not located at a higher sales volume as suggested by A&S. The authors are correct, however, in the observation that the time value of money is “largely absent in any discussion of the equity of contracts in the recorded music trade.” The framework presented in my paper provides an opportunity for an analysis of this and other important factors that constitute the complex machinations of the recording industry. Economic modelling is by its very nature a simplification, the process of abstraction from reality (making simplifying assumptions) to develop a framework within which to evaluate the behavior of key variables. Thereafter, we relax our simplifying assumptions, moving away from the abstract toward reality by introducing more variables and greater detail. This is the challenge and opportunity for future work and it is en-couraging that A&S have signalled intent to further investigate financial risk in the music industry.

Distribution of Risk and Return

The second point made by A&S relates to the uncertainty associated with new sound recording title releases in which approximately one in ten are supposedly financially successful. My paper illustrates how the existence of risk, and numerous failed investments, means that record companies must defray this cost with income generated from financially successful titles. A&S assert, “The implication is that successful artists are ultimately financing less successful ones.” They describe as impractical the notion of risk sharing where “artists agree to apportion royalties to defray the potential losses [associated with risk] […] helping the label minimize the cost of artist royalties.” Firstly, I do not contend that the successful artist per se subsidizes less successful ones, but rather that the record label’s share of income generated from sales of successful titles is used to cross-subsidize unsuccessful releases. The latter are essentially high-risk speculative investments akin to oil drilling where one successful strike pays for numerous unsuccessful investments. The risk factor λ is not imposed on the successful artist as suggested by A&S, but instead, enters the record company’s cost function (Equation 7, p. 97) as a separate cost element as follows:

TC = λ + TFC + MC.Q (7)

The element λis used to capture the risk and associated cost of numerous failed investments within the label’s portfolio of investments. Its inclusion in the cost function for a title-specific investment recognizes the reality that a portion of revenue from successful titles is required to cover losses on failed investments. The objective here was to demonstrate that this resulted in a higher breakeven sales volume for our multi-product firm. Accordingly, revenue captured by λ can be thought of as a contingency fund, not so much for unforeseen events but for the predictable failure of numerous releases within the label’s portfolio of annual investments. For the A&S comment to be valid, the element λwould need to be subtracted directly from the artist royalty (represented in Equation 7 as marginal cost, MC).

Secondly, with respect to the practical application of the risk-sharing model, I concur with A&S that it is unlikely to be adopted, particularly for established record labels for which accounting practices can be described as clandestine. However, it is important to note that the remuneration model proposed in my paper identified three stages over which a (variable) fraction κ was applied to the artist royalty, expressed in Equation 8 as follows:

Π = PPD – (MPC + DIST + RM +κR) (8)

It was proposed that, at sales volumes below the breakeven point κ= 0, while κ < 1 beyond the breakeven point, and finally κ = 1 for sales beyond the recoupment volume of sales. I then go on to say:

“The value of κbetween the breakeven and recoupment points would be negotiated between the parties and would ensure that both the record company and artist share in the rewards of a successful title release. Its value could also reflect the need for the record company to recover losses on unsuccessful titles.” (p. 99)

In other words, the value κcan be adjusted by mutual agreement. It is at this point that the A&S contention of impracticality is appropriately focussed. However, the discount applied to the artist royalty is not central to the remuneration model itself. As demonstrated by the preceding extract, the value of κcould also reflect the need for the record company to recover losses on unsuccessful titles. In the ensuing numerical illustration, I do provide for a discount on the value of κto compensate the record company for the risk inherent in multiple title releases.

Is it realistic to canvass this extension to the remuneration model? In negotiations of any kind it is often necessary to concede some ground in order to occupy another space. In the illustration of the remuneration model, artists would agree to receive less than the full royalty beyond the recoupment level of sales (and the full rate at some mutually agreed level beyond that) in exchange for record company agreement to pay a fraction of artist royalties prior to the recoupment sales level. This means that artists receive an income stream prior to being recouped, at the cost of a reduced (and uncertain) future income stream. As A&S rightly point out, the present value of money is higher than the future value, and even more so if the income stream is uncertain. Moreover, I would envisage that such a negotiation would include the payment of a higher royalty (κ > 1) at some mutually agreed sales volume (for example, when the title-specific target profit or rate of return has been achieved). I would imagine then that there would be many emerging artists (and their business advisors) that would find this proposition attractive, and that the driving force for its adoption would be self interest rather than altruism. Notwithstanding the above, the A&S comment has made me revisit this issue and encouraged a further exploration of earlier ideas, some of which I will briefly share here.

The Future Value of Breakeven Revenue for a Multi-Product Firm

Let us explore the first of the A&S points: that the recording advance is a fixed cost with an opportunity cost. Perhaps the best analogy to investing in a new sound recording title can be found in the pharmaceutical industry. Like investments in new titles by record labels, drug companies target R&D investments on the basis of an evaluation of potential future income. This selection process is made with imperfect information, and the uncertainty gives rise to considerable risk. The expected revenue stream will be discounted by the risk that the investment will fail to produce a product of merchantable quality. A simple numerical illustration of the breakeven point, utilizing a somewhat different approach to that presented in my earlier paper, is helpful.

First, it is helpful to distinguish between fixed cost and title establishment costs. For simplicity, my earlier paper implicitly assumed that these two components were combined and represented as fixed cost (see Equation 1, p. 91). Fixed costs are unavoidable and include rent, utilities, wages, and so forth—commonly referred to as overheads. I define establishment costs here as those related to the creation, development, and marketing of a new product—in this example a new wonder drug. Unlike expenditure of buildings and machinery, this is a sunk cost that is unrecoverable once expended. A drug company (like a record label) is a multi-product firm with a set of investments of varying value (not all recording advances are equal) and a corresponding variety of expected revenue streams. This means that fixed costs need to be apportioned across each investment using a somewhat complicated weighted formula, the formulation of which is best left for another occasion. For simplicity I will assume a set of new investments (ten new drugs) of equal value (say $1 million) totalling $10 million so that fixed costs are distributed equally across each investment. Assume also a fixed cost of $10 million per time period (per annum) that would be apportioned equally across each of the ten new drugs (at $1 million each). If one in ten new drugs is successful, the risk factor is extremely high with the probability of success equal to ten percent. This means that the breakeven revenue stream for these speculative investments is $10 million ($1m/0.10), and this covers only establishment costs. Like the A&R activity in the music industry, failed R&D in the drug industry often produces no income whatsoever.1 Accordingly, the revenue stream of the one successful drug must generate the breakeven revenue stream (in the example above, $10 million). Factoring in fixed and variable costs, the breakeven revenue is considerably higher.

The reality is of course more complex than this. For example, our drug company owns patents on a number of established drugs that generate an ongoing revenue stream for the duration of the patent (monopoly supply). This is analogous to the music catalog of the record label. Accordingly, fixed costs would need to be apportioned across all products, new and established. Moreover, given the lengthy development cycle (the time from the initial investment to market entry) this future revenue stream needs to be discounted to account for the time this money has been tied to the investment. In the pharmaceutical industry the development cycle can be up to ten years, inclusive of trials and government approvals. In the music industry, the analysis is somewhat more complicated because “failed” investments can still produce a revenue stream that can contribute to establishment costs and overheads. To illustrate let us turn our attention back to music.

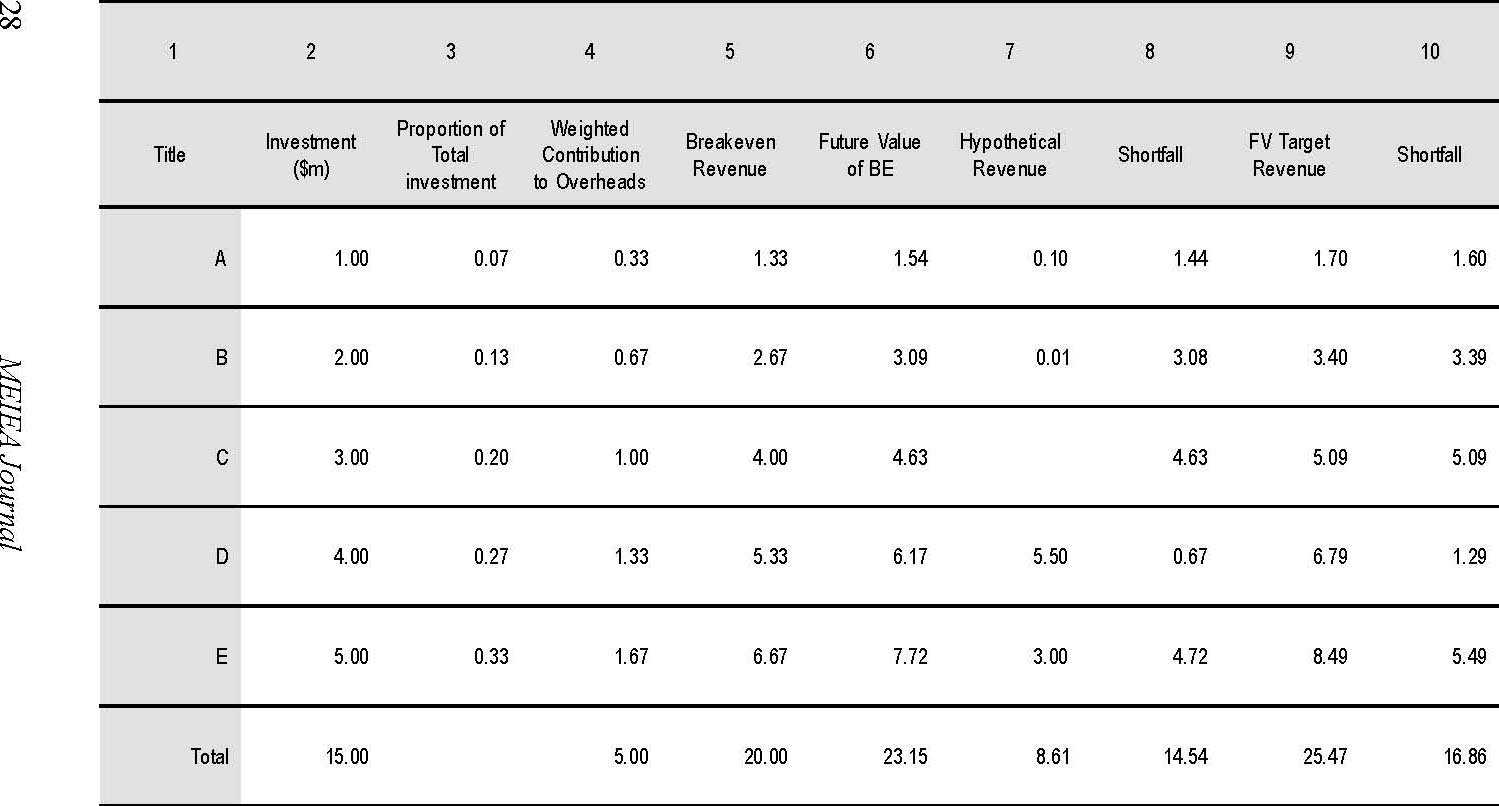

Table 1 presents data relating to a series of hypothetical A&R investments in new sound recording titles (emerging artists). For ease of exposition our investment portfolio includes five new titles (A to E) with investment (establishment cost) graduating successively by $1 million from $1 million up to $5 million (column two). Putting aside the revenue of back catalog, let’s assume the label has overheads of $5 million (fixed cost) per time period.2 Column three presents the ratio of each title-specific investment to total investment for the period ($15 million), and is used to calculate the weighted contribution to overheads (column four) required from each investment. For example, the investment of $3 million in title C repre-sents twenty percent of the total investment ($3m/$15m) and should therefore contribute $1 million to total costs (twenty percent of $5 million).

To incorporate the time value of money along the lines suggested by A&S, we need to consider the length of the development cycle and the behavior of the ensuing revenue stream. The development cycle varies across titles and I assume here a period of two years from A&R to market entry. The timing and quantum of the revenue stream is somewhat more complicated. For a new wonder drug that has been approved and is ready for market, we can estimate the future revenue stream based on the number of people with the ailment and capacity to pay. The projected revenue stream will be relatively stable (subject to the development of competing substitutes) over the term of the patent, and lower beyond that point (as competing generic brands enter the market). The parallel in music is the investment in surrogate bands or artists—those that deliberately appropriate the sound and image of an established band or artist with a proven market. This is akin to brand proliferation in the soaps and detergents industry in which copycat brands are developed to regain market share.

For a sound recording title, the product life cycle is relatively short and displays the characteristics of a fad or fashion product. The revenue stream is “chunky” and typically concentrated within the first year of release. For the purpose of calculating the future value of breakeven revenue (FVBE) for this illustration, I assume that the label aims to achieve the profit target within the first year of release (while acknowledging that it will continue to generate revenue as back catalog and contribute to overheads thereafter). Column five presents BE revenue in constant dollars while Column six presents the FVBE for the three-year period (incorporating the two-year development cycle and one-year product cycle assumptions). For example, the FVBE revenue for title C rises from $4 million to $4.63 million (compounded annually at five percent over three years)3, while the FVBE for the period (all investments) is $23.15 million, of which $3.15 million represents the opportunity cost to the label of undertaking these speculative investments. An added complication is that, unlike the drug industry, unsuccessful titles will generate a variety of unpredictable revenue streams, not necessarily related to the size of the initial investment or product quality.

To illustrate the implication of unpredictable revenue streams, let us now assume that title C is the label’s only hit record, while the other titles have varying levels of market success. Column seven presents a series of hypothetical revenue streams for each title, excluding title C. The sum of these revenue streams is $8.61 million, which exceeds the label’s overheads ($5 million) by $3.61 million. Subtracting the value of the label’s investment portfolio ($15 million for all titles), we have a shortfall of $11.39 million (constant dollars) after accounting for the revenue of all other titles. Importantly, while the unsuccessful titles are disappointing (from both the financial and artist development perspective) and fall short of their respective FVBE revenue, this illustration demonstrates that these titles can nonetheless make an important contribution to the label’s overheads and overall profitability. It is at the A&R stage that labels compete to sign emerging artists, the selection of which will determine the relative success of a label’s overall investment portfolio. Each title-specific investment is a gamble, and failing superstardom, new titles can nonetheless generate revenue and contribute towards overheads and company profits despite falling short of the title-specific breakeven point.

Given these unsuccessful titles, what is the amount of revenue that title C must generate for the label to breakeven? Column eight presents the shortfall of title specific investments (FVBE less hypothetical revenue). For example, the hypothetical revenue generated from title D ($5.5 million), while substantial, falls short of the FVBE by $0.67 million. The sum of the shortfall in revenue across all titles (excluding title C which has deliberately been set to zero) is $14.54 million. This is the FV of sales revenue that title C must generate for the record label to breakeven.4 This is considerably higher than the title-specific FVBE of $4.63 million but lower than the investment portfolio FVBE of $23.15 million.5

Of course, record companies are in the business of making profits and are accountable to shareholders looking to maximize return on investments. Let us assume that the label sets itself a target rate of return (r) of ten percent. Column nine presents the FV Target Revenue (FVTR) required to achieve the target r, and is obtained by applying a ten percent markup to the FVBE for each title. The sum of the FVTR, $25.47 million, represents a ten percent return on an investment of $23.15 million. As already noted, not all titles will achieve the FVBE let alone the FVTR. Following the same procedure for identifying the FVBE for title C, using the hypothetical revenues for all other titles, we can now identify the FVTR necessary for title C to deliver the target profit that represents a rate of return of ten percent across all investments. Column ten presents the shortfall of hypothetical revenue from titles A, B, D, and E over the FVTR (with title C again set to zero). The sum of this shortfall ($16.86 million) is the revenue from the hit record, title C, to achieve the target profit and rate of return. The target sales volume (number of albums sold) can be estimated by simply dividing the FVTR by the Value of Sale (unit price less variable costs).6

Conclusion

This hypothetical illustrates how record labels need to utilize revenue from successful titles to cross-subsidize speculative investments in other titles. As noted, the dynamics for a multi-product firm are complex, but the illustration does help to focus on some of the underlying fundamentals of financial risk in recorded music. The approach adopted in this illustration also provides a useful tool in developing problem-solving activities for music business students. For example, one activity could involve a sensitivity analysis (utilizing a simple Excel spreadsheet) whereby groups of students investigate the impact on the FVBE and FVTR by varying the underlying parameters (risk, hypothetical revenues, target rate of return, length of development cycle, etc.). For example, after assigning differential risk levels for mainstream artists (30%), surrogate artists (20%), and an artist from an emerging genre (5%), students could explore the appropriate allocation of investment funds across these titles and, given a set of hypothetical revenue streams, could explore the implications for the FVBE and FVTR necessary to achieve the label’s profit target.

I have written more on this issue than I originally intended but found myself immersed in the subject matter once again. For this, I owe a debt of gratitude to Alhadeff and Sosnick for their examination and comments on my earlier work. Academic discourse of this nature is to be encouraged and is one of the objectives of the MEIEA Journal. Alhadeff and Sosnick are to be applauded for initiating this process. I look forward with enthusiasm to their continued contribution to research in music industry financial risk.

Table 1. Hypothetical Investment Portfolio (in millions of dollars)

Endnotes

1 Citing SoundScan data Marcone (2005) reveals that 58% of new albums released in 2004 sold less that one hundred units each, while 81% sold less than one thousand units each.

2 Alternatively, we could think of revenue from back catalog covering all but $5m of fixed cost. This would be the portion of fixed cost allocated to new investments.

3 Interest on loans will typically compound daily rather than annually so the FVBE will be even higher. Offsetting this is the fact that the investment will be expended over a two-year period rather than at the commencement of the period as depicted. It is also important to note that the hypothetical revenue depicted in column seven is a stream rather than a lump sum received at the end of the period.

4 For ease of exposition, variable costs (including publishing and artist royalties) have been excluded from this illustration. Accordingly, $14.54 million is the FVBE after variable costs have been paid.

5 The implicit probability of success is twenty percent, or one title in five (1/5= 0.20). Coincidentally, since investment in title C represents twenty percent of a total investment ($1m/$5m), the FVBE for the investment portfolio, $23.15 million, is equal to the title specific FVBE divided by the risk factor ($4.63m/0.2 = $23.15m).

6 As illustrated in my paper on recoupment practices, this itself is somewhat difficult as the variable costs change over the relevant output range (for example, as a result of varying royalty rates over sales thresholds).

References

Alhadeff, Peter and Barry Sosnick. “Record Labels, Artists, and Finance: A Contribution to the Economic Analysis of Costs and the Equity of Recoupment Practices in the Music Industry.” MEIEA Journal, 5, no. 1 (2005): 13–17.

Marcone, Stephen. “Album Release Analysis: ‘New’ Albums,” Music & Entertainment Industry Educators Association Annual Conference, University of Miami, April 2005.

Papadopoulos, Theo. “Are Music Recording Contracts Equitable? An Economic Analysis of the Practice of Recoupment.” MEIEA Journal 4, no. 1 (2004): 83–103.

THEO PAPADOPOULOS is a member of the Institute of Community Engagement and Policy Alternatives and Program Director of Bachelor of Business–Music Industry at Victoria University, Australia. Papadopoulos is an experienced educator and author of numerous training materials, books, and research articles. He is a member of the FReeZACentral Management Committee and responsible for all program evaluation and reporting requirements to the funding body (Department for Victorian Communities, Australia).